- Way.com and Union Credit have partnered up to make auto loans through credit unions even more attractive.

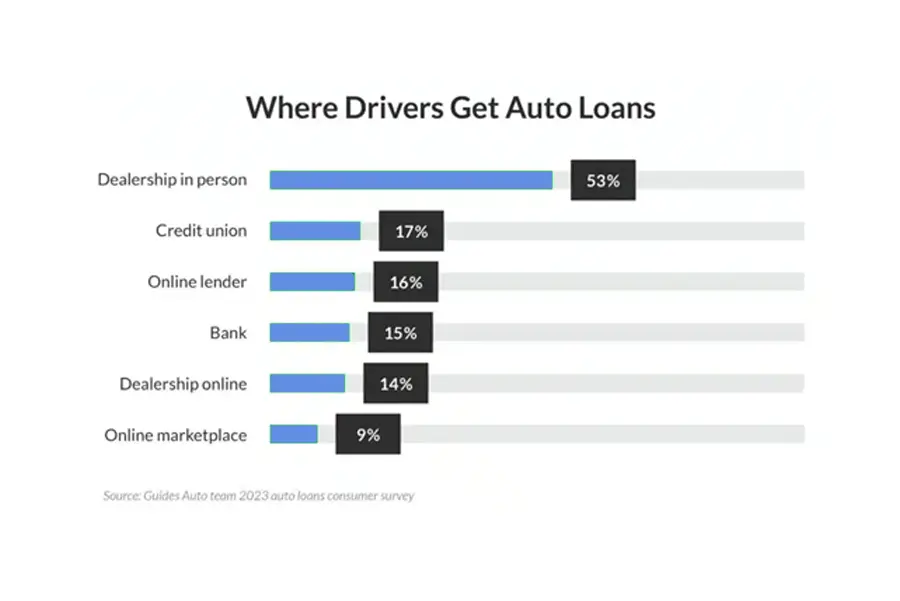

- Most people still get their auto loans from a dealership in person. Will moves like this partnership help auto loans through digital channels become more popular?

For those in the market for a new car or refinancing a loan for one they’ve already purchased, money generally comes from banks, but credit unions are also another major player in the space. In fact auto lending is a major chunk of how credit unions make money. Due to the impact auto loans have on a credit union’s bottom line, they often outdo banks in this lending sector.

However this competitive edge is thrown into sharp relief in the current inflationary market that is being combated by interest rate hikes. Credit unions put up tough competition due to the lower rates they offer compared to banks. For example, the average rate offered by credit unions for used cars was 5.94% where banks are offering 8.36% on similar loans.

These numbers allow customers to access competitive rates when it comes seeking funds for their new rides. Way.com and Union Credit have partnered up to make auto loans through credit unions even more attractive. Way.com provides customers with a slew of car services across the lifetime of an auto purchase, from finding free quotes on car insurance, airport parking, and car wash deals to auto loan refinancing.

Its partnership with Union Credit, the fintech startup allows customers to access one-click offers on car loans that are pre-approved. According to the CEO of Union Credit, Dave Buerger, this partnership is a win-win situation for both the customer and the credit union, because it eliminates the need to manually compare offers and apply for approval on part of the customer, effectively curtailing decision fatigue. It also allows credit unions to access a customer base that goes beyond their existing members.

How does it work?

To provide pre-approval, Union Credit works with TransUnion as their data provider. “We can use TransUnion’s trending credit attributes, algorithms, and fraud tools to help our participating lenders intelligently evaluate creditworthiness,” said Buerger. This allows the rates offered to consumers to be tailored to their needs and financial situation, and keeps them in a state of “perpetual approval” Buerger.

It doesn’t end at financing a car. The partnership offers parallel products such as warranties and insurances. According to Buerger, this is a key piece of doing auto lending digitally. “Warranties and insurance products portray that if there is an issue, a faulty item will be fixed or replaced. When consumers shop online – particularly for expensive products – they need to feel confident that they are making smart purchases of products that will last. Offering access to parallel products helps boost non-interest income and establishes your credit union as a one-stop shop for financial needs.”

Tearsheet Take: En route to digital auto lending

In 2018, only 5% of consumers applied for an auto loan online. This number has grown over the span of the last 5 years. Online channels are starting to take off in the sector – 16% of car buyers get their loans via an online lender, 14% get them from a dealership online, and 9% use online marketplaces for the purpose. Cumulatively, 39% of auto loan originations come from online channels. Conversely, 17% use credit unions and 53% get auto loans from a dealership in person.

Getting auto loans from a dealership in person has historically been a popular choice. But steadily, this number is declining, down from 73% in 2018.